The short answer

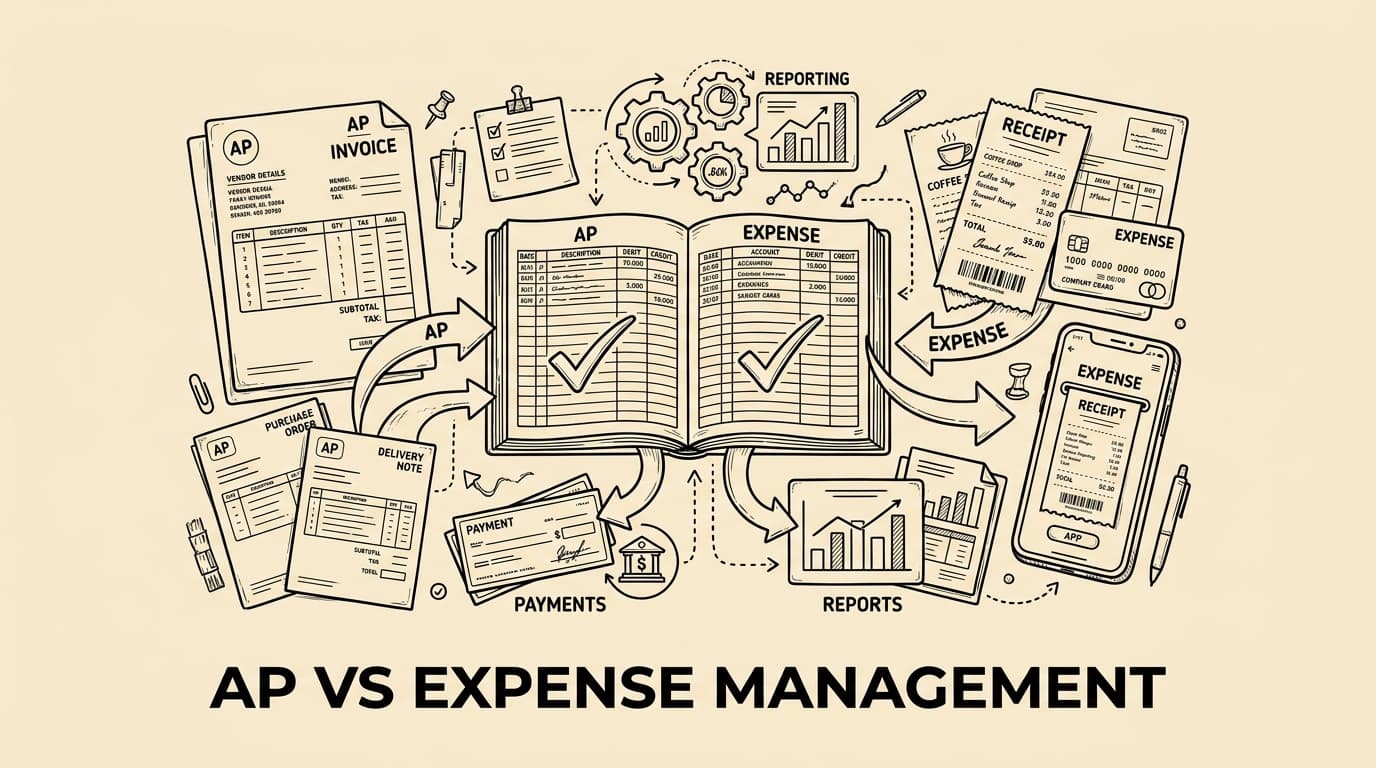

Accounts payable and expense management both sit in finance operations, but they solve different control problems. Accounts payable is primarily about money owed to suppliers: invoices, purchase orders, payment terms, vendor records and the liability that remains until the supplier is paid. Expense management is about employee-initiated spend: card charges, reimbursements, mileage, travel receipts and policy checks before the amount is booked or paid back to the employee. Confusing the two creates slow approvals, duplicate records and unclear ownership at month end.

A practical boundary helps teams decide which workflow, tool and approval logic should handle each transaction. If the document comes from a supplier and relates to goods or services bought by the company, it usually belongs in accounts payable. If the spend starts with an employee using a card, paying personally, travelling, entertaining a client or claiming mileage, it usually belongs in expense management. The handover matters because both streams eventually affect the general ledger, cash forecasting and audit evidence.

Side-by-side comparison

| Area | Accounts payable | Expense management |

|---|---|---|

| Typical source | Supplier invoice | Employee receipt, card feed or claim |

| Main risk | Wrong supplier, duplicate invoice, payment error | Policy breach, missing receipt, wrong tax treatment |

| Primary approver | Budget owner or purchasing owner | Line manager plus finance review |

| Output | Approved invoice and payment | Approved expense entry or reimbursement |

What accounts payable covers

Accounts payable starts when the company has received goods or services from a vendor and owes money for them. The AP team normally manages supplier master data, incoming invoices, purchase-order matching, invoice coding, payment scheduling, remittance information and supplier questions. In many organisations this is part of a procure-to-pay flow. The key document is the vendor invoice, not the employee receipt. The control question is whether the supplier invoice is legitimate, complete, approved under purchasing rules and ready to pay under agreed terms.

Because AP represents a liability, timing matters. The invoice may be approved today but paid next week or next month according to supplier terms. Finance teams use AP ageing, payment runs and cash forecasts to decide which obligations need attention. AP automation can remove manual data entry and route invoices to budget owners, but the process is still supplier-centred. It answers: do we owe this external party money, how much do we owe, which cost centre should carry it, and when should we release cash?

What expense management covers

Expense management starts closer to the employee. A consultant pays for a train ticket, a sales manager uses a company card for a hotel, a founder buys SaaS with a card, or an engineer claims mileage after visiting a customer. The transaction may not arrive as a supplier invoice addressed to the company. Instead, finance receives a receipt, card feed, mileage log or reimbursement request. The control question is whether the spend is business-related, policy-compliant, properly substantiated and assigned to the right project, customer or cost centre.

For international teams, expense management also handles local tax evidence, currencies, per-diem rules, card controls and receipt retention. The process usually includes employee submission, manager approval, finance review, export to accounting and reimbursement or card settlement. Tools like Bill.Dock focus on this employee-spend layer: capturing receipts, classifying expenses, applying approval rules and keeping a clean audit trail before the data reaches accounting. It should complement, not replace, a mature AP process.

A clear decision rule

The simplest decision rule is source plus ownership. Supplier sends invoice to the company: route to AP. Employee creates, pays or substantiates the spend: route to expense management. Edge cases still exist. A hotel may send an invoice to the company for a group booking, which fits AP. The same hotel stay paid by an employee card fits expense management. A software subscription billed to a central procurement account fits AP; an employee buying a low-value tool on a virtual card may fit expense management until finance consolidates subscriptions later.

This boundary prevents duplicate payments. Without it, an invoice may be paid through AP while the employee also submits a receipt for reimbursement, or a card transaction may be coded twice because AP sees a supplier statement later. A documented routing rule should define the evidence required, the approver, the accounting export and the exception path. Finance does not need a perfect taxonomy; it needs a consistent one that people actually use.

Controls and approvals are different

AP approvals focus on supplier legitimacy, budget ownership, purchase orders and payment authority. The approver is often the person who requested the purchase or owns the budget. Controls may include vendor onboarding, bank-detail changes, duplicate invoice detection, three-way matching and payment-run separation. These checks are designed to protect the company from paying the wrong supplier, paying twice or paying without receiving what was ordered.

Expense approvals focus on policy and context. Was the meal within the policy limit? Is the taxi justified? Does the receipt show date, amount and merchant? Is VAT recoverable? Did the employee attach enough evidence for the jurisdiction? The approver may be a line manager rather than a procurement owner. Finance then checks coding, receipt quality and tax treatment. Treating these approvals as identical usually slows both teams because supplier invoices and employee claims need different questions.

Data, tax evidence and audit trail

Both processes need strong audit evidence, but the evidence looks different. AP stores supplier invoices, purchase orders, delivery notes, contracts and payment confirmations. Expense management stores receipts, card transactions, mileage logs, policy decisions and approval comments. EU VAT rules recognise electronic invoices as equivalent to paper invoices under defined conditions, while national rules can add local requirements. For employee reimbursements, tax authorities often care about substantiation: date, amount, business purpose and whether excess reimbursements are returned or treated correctly.

A clean audit trail links the transaction to the right decision. In AP, that may mean invoice number, supplier VAT ID, approval timestamp and payment batch. In expense management, it may mean original receipt image, OCR data, employee declaration, manager approval and accounting export. The audit trail should show not only what was booked but why it was accepted. This is where specialised expense tools reduce end-of-month archaeology: they capture context at the moment the employee still remembers it.

Where the two processes meet

The two streams meet in accounting, cash management and reporting. Both need cost centres, ledger accounts, VAT codes and project dimensions. Both may feed the same ERP or accounting system. Finance leaders should therefore design a shared chart-of-accounts mapping and reporting vocabulary while keeping operational workflows separate. The goal is not to build two disconnected silos. The goal is to let each process collect the right evidence before sending standardised data downstream.

A common integration pattern is to let AP automation handle vendor invoices and payment runs, while an expense-management platform captures employee spend and exports approved entries to accounting. Company-card feeds can be reconciled inside the expense tool and then posted as journal entries or card liabilities. Reimbursements can be exported to payroll or payments depending on the country and policy. The handover should be documented so controllers know where to investigate when numbers do not reconcile.

Implementation checklist for finance teams

Start with a transaction map. List the ten most common spend types in your business: supplier invoices, subscriptions, travel, meals, mileage, home-office equipment, event costs, professional services, card charges and cash reimbursements. For each one, decide the owner, evidence required, approval path, accounting export and payment method. Then publish the rule in plain language. Employees do not need a finance textbook; they need to know which button to press and what receipt to keep.

Next, separate the approval logic. AP should not wait for line managers to explain every receipt, and employees should not be forced into a purchase-order workflow for a taxi fare. Configure thresholds, categories and exceptions around the real risk. A low-value coffee receipt may need automatic policy validation; a new supplier bank account needs stronger segregation of duties. Finally, review month-end corrections. If the same corrections repeat, the boundary or coding rule is probably unclear.

Common mistakes

One mistake is using AP software as a generic inbox for all spend. It may capture documents, but it often lacks employee-level policy checks, card matching and receipt nudges. Another mistake is treating expense management as a lightweight AP substitute. Employee receipts are not the same as supplier invoices, and reimbursement approval does not replace vendor onboarding or payment controls. A third mistake is letting departments invent their own exceptions. Once teams start bypassing the defined route, duplicate claims and missing evidence become much harder to detect.

The most expensive mistake is waiting until audit or month end to discover the gap. If finance cannot quickly answer whether a transaction was a supplier invoice, a card charge or a reimbursed employee expense, reporting becomes slower and less reliable. Strong processes make the answer visible from the start. They also reduce frustration because employees, managers and AP specialists stop forwarding the same document between systems.

FAQ

Is accounts payable the same as expense management? No. AP manages supplier liabilities and invoice payments. Expense management manages employee spend, receipts, cards and reimbursements.

Can one tool handle both? Some suites cover both areas, but the workflows still need separate rules. The important point is whether the tool captures the right evidence and approvals for each spend type.

Where do company cards belong? Company-card transactions usually fit expense management because an employee creates the spend and must attach context. The card liability or settlement may later be reconciled in accounting.

What should be automated first? Automate the process with the most leakage or manual work. For many growing teams that means receipts, card matching and approval reminders; for invoice-heavy companies it may be AP capture and matching.

How does Bill.Dock fit? Bill.Dock supports the employee-spend side: receipt capture, expense classification, approval evidence and export-ready records for finance.

Conclusion

Accounts payable and expense management are neighbours, not twins. AP protects the supplier-invoice and payment process. Expense management protects employee-initiated spend before it becomes an accounting entry or reimbursement. When finance defines the boundary, teams gain faster approvals, cleaner books and fewer awkward month-end questions. The best setup is usually not one giant workflow; it is two specialised workflows with a clear handover into the same finance system.