Mileage looks simple until several employees submit different kinds of journeys: client meetings, airport transfers, site visits, home-office errands and mixed private routes. A policy turns those journeys into a consistent finance process rather than a negotiation at month end.

The aim is not to make reimbursement harder. It is to make every claim answer the same questions before finance has to ask them: who travelled, when, from where to where, why the trip was business related, which vehicle type was used and which rate applies.

Define eligible journeys before defining the rate

Start by naming the business purposes that are reimbursable. Client visits, supplier meetings, project-site inspections, bank or tax appointments and approved training trips are usually straightforward. Ordinary commuting between home and the normal workplace should normally be excluded unless local rules or a written exception apply.

This distinction matters because tax authorities treat private, commuting and business mileage differently. HMRC, the IRS and European tax administrations publish rules or rates that change over time, so the policy should reference the current official table rather than hard-coding a stale number into the article or employee handbook.

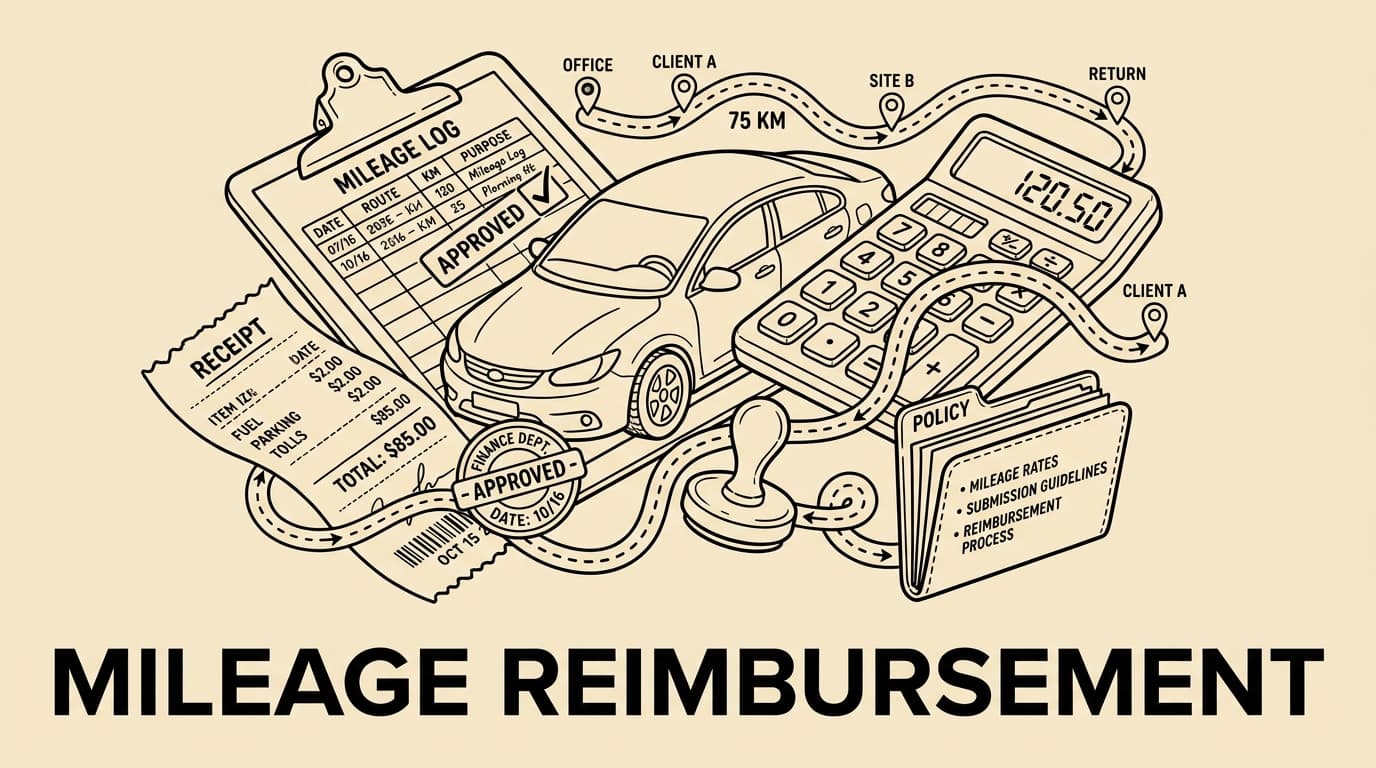

Set the evidence standard

A reliable mileage claim records the date, start and end point, business purpose, distance, vehicle category and any passenger or toll information required by the company. Odometer readings are helpful where rules demand them, while map-based distance can be enough for low-risk local trips if the policy says so.

Finance teams should reject vague lines such as ‘customer trip’ or ‘sales visit’ when the location and purpose are missing. A short rejection message is fairer than approving weak evidence and trying to reconstruct the route during an audit months later.

Keep the policy source-linked: rate tables belong to tax authorities and payroll advisers, while the company policy should describe the workflow, evidence and exceptions. This also keeps the rule stable when fuel prices, vehicle mixes or tax guidance change during the year.

Choose a reimbursement model

Most employers use one of three models: an official tax-authority rate, an internally approved rate below that ceiling, or actual-cost reimbursement for special fleets. The official-rate model is easiest to administer because employees recognise it and finance can update it once per year.

Actual-cost models can be justified for unusual vehicles or project work, but they create more evidence work because fuel, insurance, maintenance and private-use allocation must be separated. For ordinary employee cars, a simple per-mile or per-kilometre policy is usually easier to explain and control.

Build approval controls into the workflow

Mileage controls should be preventive, not only detective. Require a manager to approve the business reason, let finance validate the rate and distance, and flag duplicate routes or weekend claims for review. The reviewer should see the policy rule next to the claim, not in a separate PDF.

Tools like Bill.Dock help by keeping receipts, claim context and approval comments together. The value is not only faster reimbursement; it is a cleaner evidence trail when finance has to show why a claim was accepted, corrected or rejected.

Keep the policy source-linked: rate tables belong to tax authorities and payroll advisers, while the company policy should describe the workflow, evidence and exceptions. This also keeps the rule stable when fuel prices, vehicle mixes or tax guidance change during the year.

Handle international and remote teams

International teams need local appendices. A UK employee, a German employee and a Danish employee may all use a private car for business, but tax treatment, documentation language and record-retention practice are not identical. A central policy should therefore define the control model and let local payroll or tax advisers maintain country-specific rates.

Remote work adds another complication: the employee may start from home, a coworking space or a temporary project address. The policy should state which location counts as the normal work base and when a trip from home becomes reimbursable business travel.

Mileage, VAT and receipts

Mileage reimbursement is not the same as a fuel receipt. In many jurisdictions the employer needs a proper invoice or receipt to reclaim VAT on fuel or parking, while the mileage allowance compensates use of the private vehicle. The European Commission explains that EU VAT invoicing rules set common principles and national rules can add details.

Keep parking, tolls, ferries and public charging receipts attached to the same claim but classified separately. This makes VAT review easier and avoids mixing a distance allowance with direct pass-through costs.

Keep the policy source-linked: rate tables belong to tax authorities and payroll advisers, while the company policy should describe the workflow, evidence and exceptions. This also keeps the rule stable when fuel prices, vehicle mixes or tax guidance change during the year.

Fraud and error patterns to watch

The most common problems are not always dramatic fraud. They are rounded distances, repeated favourite routes, private detours, duplicated claims after a cancelled meeting and old rates used after the annual update. A monthly exception report catches these patterns before they become normal behaviour.

A fair policy also protects employees. When the rule is visible and the system checks it consistently, honest claimants are not surprised by arbitrary reductions and reviewers can focus on genuine exceptions.

Implementation checklist

Publish the policy in one page plus local appendices. Add examples for approved, partly approved and rejected journeys. Configure the expense tool with current rates, required fields and manager approval. Train employees with two realistic examples rather than a long tax lecture.

Finally, review the policy every year when official mileage rates or payroll reporting thresholds change. Mark the review owner and date in the policy so nobody has to guess whether the numbers are still current.

Keep the policy source-linked: rate tables belong to tax authorities and payroll advisers, while the company policy should describe the workflow, evidence and exceptions. This also keeps the rule stable when fuel prices, vehicle mixes or tax guidance change during the year.

FAQ

Can we reimburse below the official rate? Often yes, but the tax and employee-relations consequences depend on the country and contract. Finance should check payroll advice before changing the rate.

Do employees need receipts for mileage? They normally need trip evidence; separate receipts are needed for items such as parking, tolls or fuel where the company wants to record or reclaim those costs.

Should electric cars have a separate rule? Many companies create an appendix for electric vehicles, charging evidence and home-charging reimbursement because the cost pattern differs from petrol or diesel.

Conclusion

A good employee mileage reimbursement policy is short, current and operational. It defines eligible trips, evidence, rates, approval roles and exceptions in language employees can use on the road. Once those rules are embedded in the expense workflow, mileage stops being a recurring argument and becomes a controlled, auditable part of travel spending.

Make mileage claims easier to audit

Bill.Dock gives finance teams a structured place for receipts, mileage context, approval notes and policy checks. That means fewer follow-up messages, clearer month-end evidence and a better experience for employees who submit legitimate business travel.

Governance detail 1

For governance round 1, record who owns the policy, which tax or payroll source was checked, when the rate was last updated and how exceptions are approved. Keep this note practical rather than legalistic: finance needs enough evidence to review the claim, payroll needs enough information to report correctly, and employees need wording they can understand before they travel.

Governance detail 2

For governance round 2, record who owns the policy, which tax or payroll source was checked, when the rate was last updated and how exceptions are approved. Keep this note practical rather than legalistic: finance needs enough evidence to review the claim, payroll needs enough information to report correctly, and employees need wording they can understand before they travel.

Governance detail 3

For governance round 3, record who owns the policy, which tax or payroll source was checked, when the rate was last updated and how exceptions are approved. Keep this note practical rather than legalistic: finance needs enough evidence to review the claim, payroll needs enough information to report correctly, and employees need wording they can understand before they travel.

Governance detail 4

For governance round 4, record who owns the policy, which tax or payroll source was checked, when the rate was last updated and how exceptions are approved. Keep this note practical rather than legalistic: finance needs enough evidence to review the claim, payroll needs enough information to report correctly, and employees need wording they can understand before they travel.

Governance detail 5

For governance round 5, record who owns the policy, which tax or payroll source was checked, when the rate was last updated and how exceptions are approved. Keep this note practical rather than legalistic: finance needs enough evidence to review the claim, payroll needs enough information to report correctly, and employees need wording they can understand before they travel.

Governance detail 6

For governance round 6, record who owns the policy, which tax or payroll source was checked, when the rate was last updated and how exceptions are approved. Keep this note practical rather than legalistic: finance needs enough evidence to review the claim, payroll needs enough information to report correctly, and employees need wording they can understand before they travel.