A receipt retention policy is a small document with a large operational effect. It tells people what evidence to keep, how to capture it, where it belongs, and who follows up when something is missing. For small businesses, that clarity prevents month-end chaos, protects tax evidence, and keeps employee reimbursements fair. The policy should not pretend to replace local legal advice; it should translate advice into daily behaviour that employees, managers and finance can actually follow.

Why a receipt retention policy matters

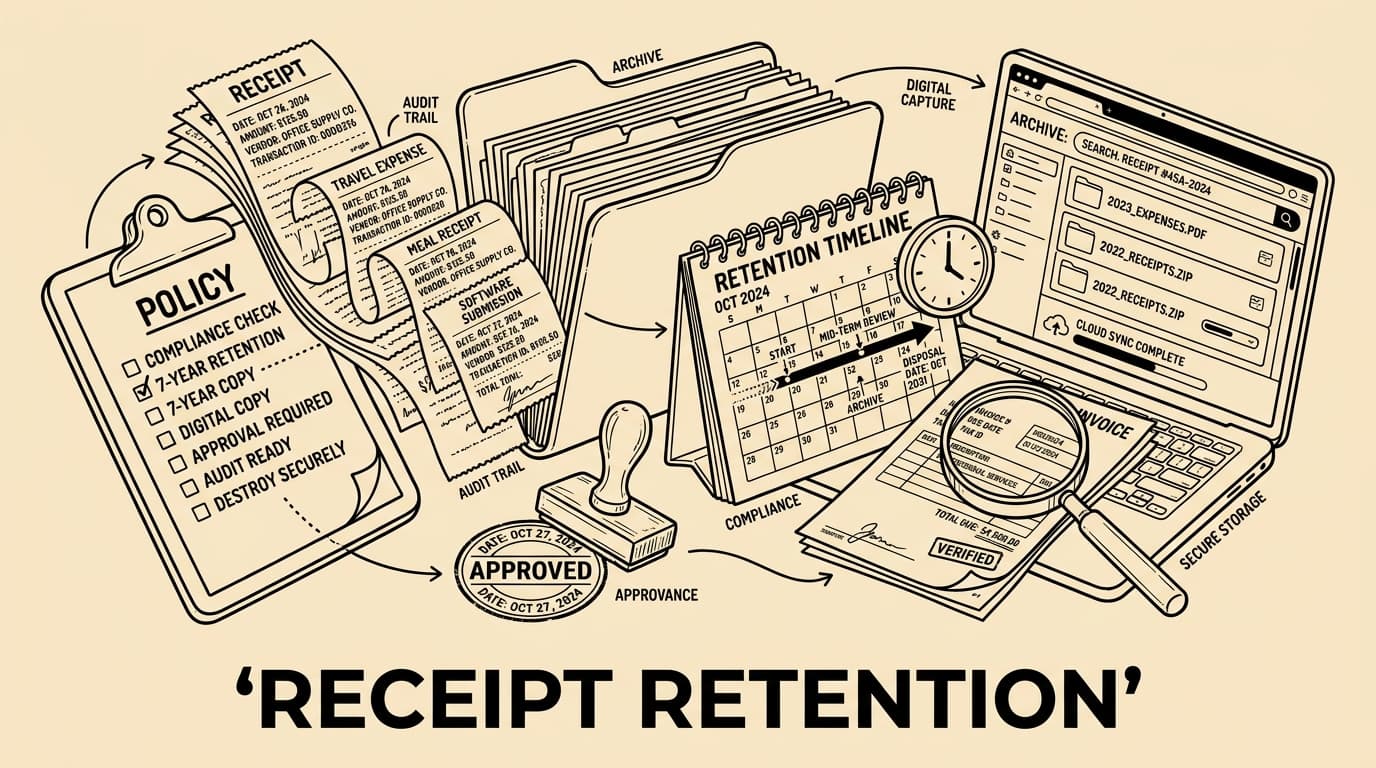

For every small business, a receipt retention policy should make the evidence chain obvious: who spent money, why it was a business cost, which receipts or invoices proves it, who gave approval, where the file is stored, and how the finance team can find it later. The practical rule is to keep policy language simple enough for employees and detailed enough for tax adviser. Why a receipt retention policy matters should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, GBP or USD, tax information where relevant, project or cost centre, business purpose, and the submitter. Use a retention matrix that your accountant or tax adviser can adapt for every country where you operate. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the audit trail stays complete.

What the policy should cover

For every small business, a receipt retention policy should make the evidence chain obvious: who spent money, why it was a business cost, which receipts or invoices proves it, who gave approval, where the file is stored, and how the finance team can find it later. The practical rule is to keep policy language simple enough for employees and detailed enough for tax adviser. What the policy should cover should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, GBP or USD, tax information where relevant, project or cost centre, business purpose, and the submitter. Use a retention matrix that your accountant or tax adviser can adapt for every country where you operate. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the audit trail stays complete.

- Receipts

- Invoices

- Business purpose

- Audit trail

Paper, email and digital receipt rules

For every small business, a receipt retention policy should make the evidence chain obvious: who spent money, why it was a business cost, which receipts or invoices proves it, who gave approval, where the file is stored, and how the finance team can find it later. The practical rule is to keep policy language simple enough for employees and detailed enough for tax adviser. Paper, email and digital receipt rules should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, GBP or USD, tax information where relevant, project or cost centre, business purpose, and the submitter. Use a retention matrix that your accountant or tax adviser can adapt for every country where you operate. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the audit trail stays complete.

Retention matrix and ownership

For every small business, a receipt retention policy should make the evidence chain obvious: who spent money, why it was a business cost, which receipts or invoices proves it, who gave approval, where the file is stored, and how the finance team can find it later. The practical rule is to keep policy language simple enough for employees and detailed enough for tax adviser. Retention matrix and ownership should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, GBP or USD, tax information where relevant, project or cost centre, business purpose, and the submitter. Use a retention matrix that your accountant or tax adviser can adapt for every country where you operate. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the audit trail stays complete.

Approval workflow and exceptions

For every small business, a receipt retention policy should make the evidence chain obvious: who spent money, why it was a business cost, which receipts or invoices proves it, who gave approval, where the file is stored, and how the finance team can find it later. The practical rule is to keep policy language simple enough for employees and detailed enough for tax adviser. Approval workflow and exceptions should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, GBP or USD, tax information where relevant, project or cost centre, business purpose, and the submitter. Use a retention matrix that your accountant or tax adviser can adapt for every country where you operate. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the audit trail stays complete.

- Receipts

- Invoices

- Business purpose

- Audit trail

Month-end controls for finance

For every small business, a receipt retention policy should make the evidence chain obvious: who spent money, why it was a business cost, which receipts or invoices proves it, who gave approval, where the file is stored, and how the finance team can find it later. The practical rule is to keep policy language simple enough for employees and detailed enough for tax adviser. Month-end controls for finance should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, GBP or USD, tax information where relevant, project or cost centre, business purpose, and the submitter. Use a retention matrix that your accountant or tax adviser can adapt for every country where you operate. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the audit trail stays complete.

Automation without losing evidence

For every small business, a receipt retention policy should make the evidence chain obvious: who spent money, why it was a business cost, which receipts or invoices proves it, who gave approval, where the file is stored, and how the finance team can find it later. The practical rule is to keep policy language simple enough for employees and detailed enough for tax adviser. Automation without losing evidence should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, GBP or USD, tax information where relevant, project or cost centre, business purpose, and the submitter. Use a retention matrix that your accountant or tax adviser can adapt for every country where you operate. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the audit trail stays complete.

Workflow table

| Step | Owner | Evidence |

|---|---|---|

| Capture | Employee | Receipt or invoice image, date, amount, merchant |

| Review | Manager | Business purpose, policy match, exception reason |

| Store | Finance | Searchable archive, category, approval timestamp |

| Export | Bookkeeping | Accounting file, audit trail, tax adviser notes |

Tools like Bill.Dock can help turn the policy into repeatable work: employees capture receipts immediately, managers see exceptions in context, and finance keeps a searchable audit trail instead of chasing files across email and chat.

FAQ

How long should receipts be retained?

Define the answer in your policy, keep a documented exception route, and review the wording with the person responsible for accounting and tax advice.

Which receipts are acceptable in a digital policy?

Define the answer in your policy, keep a documented exception route, and review the wording with the person responsible for accounting and tax advice.

Who owns receipt follow-up?

Define the answer in your policy, keep a documented exception route, and review the wording with the person responsible for accounting and tax advice.

Can automation replace a written policy?

Define the answer in your policy, keep a documented exception route, and review the wording with the person responsible for accounting and tax advice.

Conclusion

For every small business, a receipt retention policy should make the evidence chain obvious: who spent money, why it was a business cost, which receipts or invoices proves it, who gave approval, where the file is stored, and how the finance team can find it later. The practical rule is to keep policy language simple enough for employees and detailed enough for tax adviser. Month-end controls for finance should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, GBP or USD, tax information where relevant, project or cost centre, business purpose, and the submitter. Use a retention matrix that your accountant or tax adviser can adapt for every country where you operate. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the audit trail stays complete.