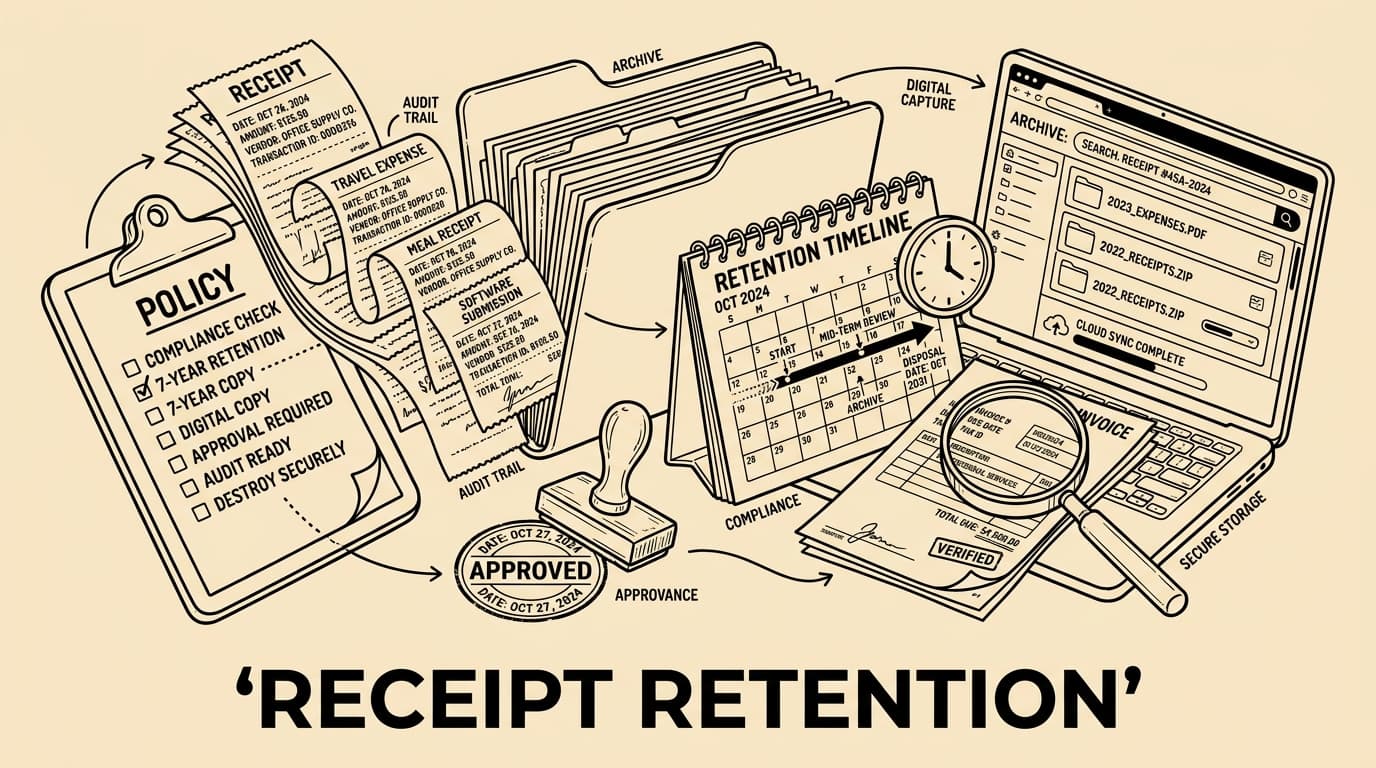

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Hvorfor kvitteringsoppbevaring er viktig should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.

Hvorfor kvitteringsoppbevaring er viktig

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Hvorfor kvitteringsoppbevaring er viktig should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.

Hva policyen bør dekke

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Hva policyen bør dekke should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.

- Kvitteringer

- Fakturaer

- Forretningsformål

- Revisjonsspor

Papir, e-post og digitale kvitteringer

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Papir, e-post og digitale kvitteringer should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.

Oppbevaringsmatrise og ansvar

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Oppbevaringsmatrise og ansvar should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.

Godkjenninger og unntak

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Godkjenninger og unntak should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.

- Kvitteringer

- Fakturaer

- Forretningsformål

- Revisjonsspor

Månedsavslutning for økonomi

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Månedsavslutning for økonomi should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.

Automatisering uten å miste bevis

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Automatisering uten å miste bevis should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.

Workflow-tabell

| Steg | Eier | Bevis |

|---|---|---|

| Fangst | Ansatt | Kvitteringsbilde, dato, beløp, leverandør |

| Kontroll | Leder | Formål, policy, unntak |

| Lagring | Økonomi | Søkbart arkiv, kategori, godkjenning |

| Eksport | Regnskap | Regnskapsfil, revisjonsspor, notat |

Verktøy som Bill.Dock gjør policyen praktisk: ansatte fanger kvitteringer raskt, ledere ser unntak i kontekst, og økonomi beholder et søkbart revisjonsspor.

FAQ

Hvor lenge skal kvitteringer oppbevares?

Definer svaret i policyen, dokumenter unntak og avklar teksten med regnskap og rådgiver.

Hvilke digitale kvitteringer godtas?

Definer svaret i policyen, dokumenter unntak og avklar teksten med regnskap og rådgiver.

Hvem følger opp manglende bilag?

Definer svaret i policyen, dokumenter unntak og avklar teksten med regnskap og rådgiver.

Kan automatisering erstatte policyen?

Definer svaret i policyen, dokumenter unntak og avklar teksten med regnskap og rådgiver.

Konklusjon

For every liten bedrift, a retningslinjer for kvitteringsoppbevaring should make the evidence chain obvious: who spent money, why it was a business cost, which kvitteringer or fakturaer proves it, who gave godkjenning, where the file is stored, and how the økonomiteam can find it later. The practical rule is to keep policy language simple enough for ansatte and detailed enough for regnskapsfører. Månedsavslutning for økonomi should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in NOK, tax information where relevant, project or cost centre, forretningsformål, and the submitter. I Norge bør policyen tilpasses bokføringsloven, Skatteetaten, mva-dokumentasjon, NOK-beløp og rådgivning. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the revisjonsspor stays complete.