For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Warum Belegaufbewahrung wichtig ist should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.

Warum Belegaufbewahrung wichtig ist

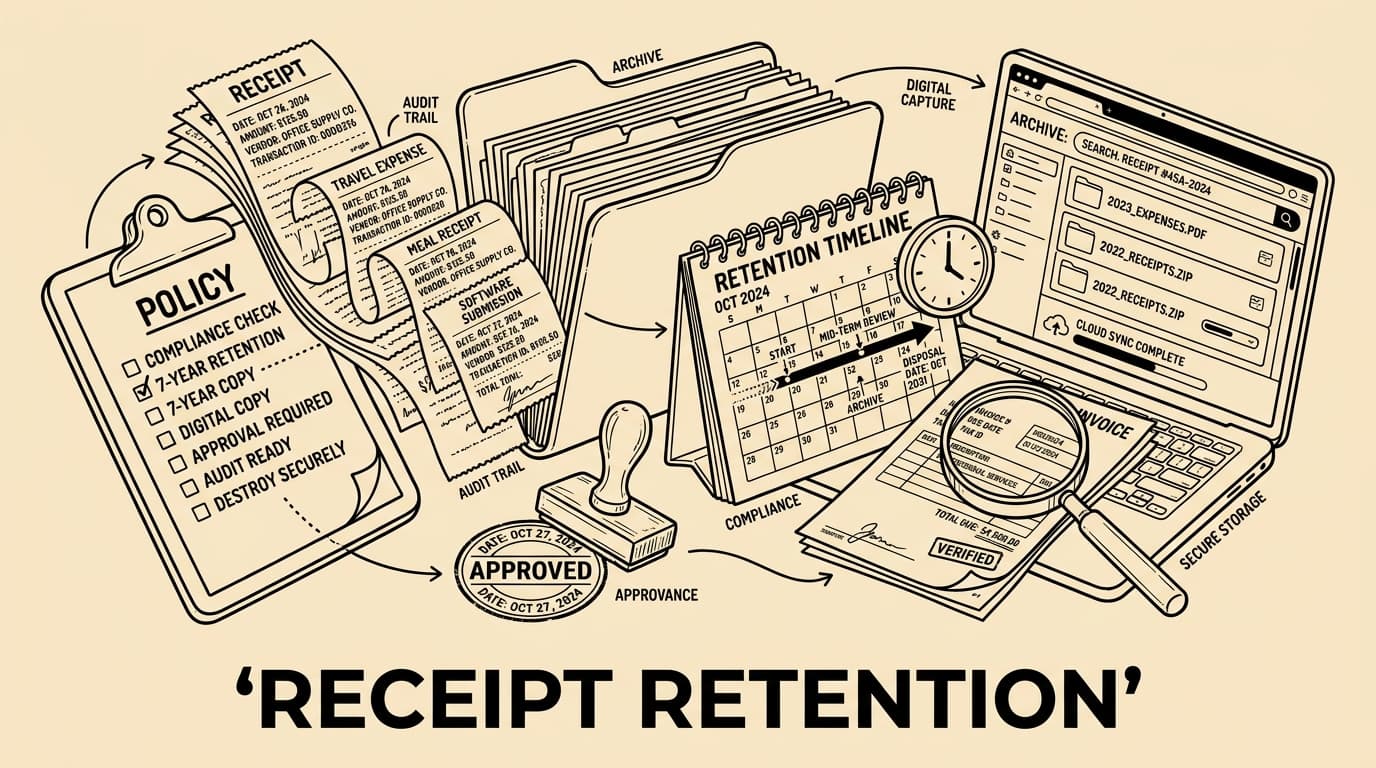

For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Warum Belegaufbewahrung wichtig ist should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.

Was die Richtlinie abdecken sollte

For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Was die Richtlinie abdecken sollte should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.

- Belege

- Rechnungen

- Geschäftlicher anlass

- Prüfpfad

Papier-, E-Mail- und digitale Belege

For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Papier-, E-Mail- und digitale Belege should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.

Aufbewahrungsmatrix und Verantwortung

For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Aufbewahrungsmatrix und Verantwortung should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.

Freigaben und Ausnahmen

For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Freigaben und Ausnahmen should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.

- Belege

- Rechnungen

- Geschäftlicher anlass

- Prüfpfad

Monatsabschluss-Kontrollen für Finance

For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Monatsabschluss-Kontrollen für Finance should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.

Automatisierung ohne Beweisverlust

For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Automatisierung ohne Beweisverlust should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.

Workflow-Tabelle

| Schritt | Owner | Nachweis |

|---|---|---|

| Erfassen | Mitarbeitende | Belegbild, Datum, Betrag, Händler |

| Prüfen | Manager | Geschäftlicher Anlass, Richtlinie, Ausnahmegrund |

| Ablage | Finance | Suchbares Archiv, Kategorie, Freigabezeitpunkt |

| Export | Buchhaltung | Buchungsdatei, Prüfpfad, Steuerberater-Notiz |

Tools wie Bill.Dock machen aus der Richtlinie einen wiederholbaren Prozess: Mitarbeitende erfassen Belege sofort, Manager sehen Ausnahmen im Kontext und Finance behält einen suchbaren Prüfpfad.

FAQ

Wie lange müssen Belege aufbewahrt werden?

Definiere die Antwort in der Richtlinie, dokumentiere Ausnahmen und stimme die Formulierung mit Buchhaltung und Steuerberatung ab.

Welche digitalen Belege sind akzeptabel?

Definiere die Antwort in der Richtlinie, dokumentiere Ausnahmen und stimme die Formulierung mit Buchhaltung und Steuerberatung ab.

Wer ist für fehlende Belege zuständig?

Definiere die Antwort in der Richtlinie, dokumentiere Ausnahmen und stimme die Formulierung mit Buchhaltung und Steuerberatung ab.

Ersetzt Automatisierung eine Richtlinie?

Definiere die Antwort in der Richtlinie, dokumentiere Ausnahmen und stimme die Formulierung mit Buchhaltung und Steuerberatung ab.

Fazit

For every kleines Unternehmen, a Richtlinie zur Belegaufbewahrung should make the evidence chain obvious: who spent money, why it was a business cost, which Belege or Rechnungen proves it, who gave Freigabe, where the file is stored, and how the Finanzteam can find it later. The practical rule is to keep policy language simple enough for Mitarbeitende and detailed enough for Steuerberater. Monatsabschluss-Kontrollen für Finance should therefore be written as a workflow, not as a legal paragraph. Define required fields such as date, merchant, amount in EUR, tax information where relevant, project or cost centre, geschäftlicher Anlass, and the submitter. Im DACH-Kontext sollten GoBD, USt-Nachweise, Aufbewahrungsfristen und Verfahrensdokumentation mit Steuerberatung abgestimmt werden. A good process also explains exceptions: lost documents, faded paper, emailed invoices, card statements, subscriptions, travel bookings, meal attendees, and reimbursements paid after the month closes. When the same rule appears in onboarding, expense software and the month-end checklist, people follow it more consistently and the Prüfpfad stays complete.